Year-by-Year Projections

See your future year-by-year with comprehensive cash flow, taxes, and account balances.

NestMint helps you model your financial future with clarity — so you can make smarter decisions, reach your goals, and enjoy what matters most.

Everything you need to plan, model, and project your financial future with confidence.

See your future year-by-year with comprehensive cash flow, taxes, and account balances.

Compare strategies side-by-side to reduce projected taxes and support lifetime wealth.

Visualize thousands of market scenarios and understand the range of possible outcomes.

Plan ahead for taxes, RMDs, and IRMAA surcharges with proactive insights.

Start strong, build smart habits, and watch your money grow.

Make informed decisions and transition into retirement with clarity.

Protect your wealth and enjoy peace of mind through every year.

Take control of your financial future with NestMint.

Already have an account? Log in

NestMint Workplace

NestMint Workplace helps employees and retirees plan for today and tomorrow with confidence.

Build a strong financial future with tools to plan, save, and stay on track.

Make informed decisions and create sustainable income in retirement.

Set goals, estimate outcomes, and build a plan that fits your future.

Model retirement income and create a withdrawal strategy you can count on.

Compare options side-by-side to find the strategy that aligns with your goals.

Explore different scenarios to prepare for life’s twists and turns.

Your information is protected with industry-leading security and privacy standards.

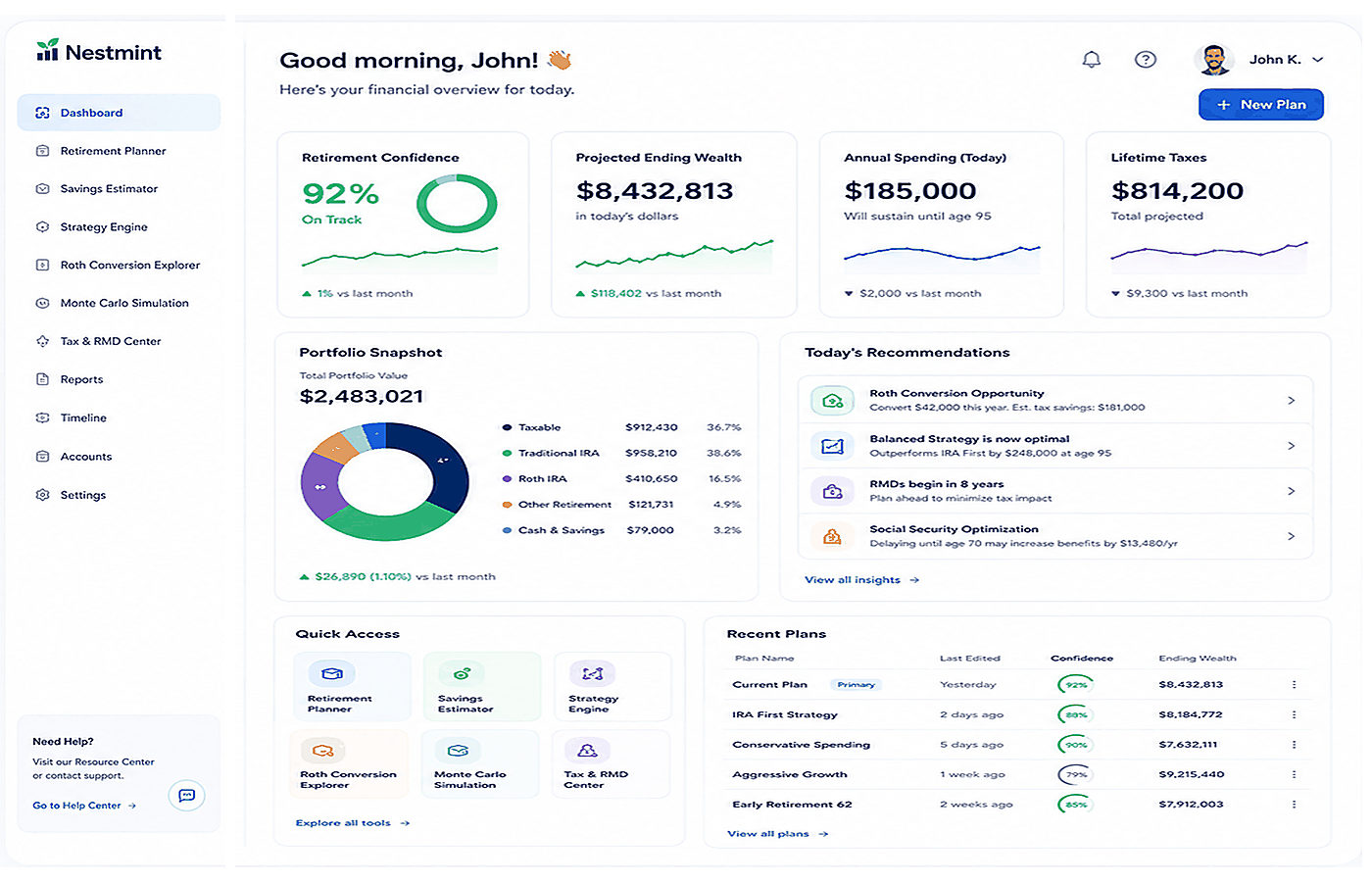

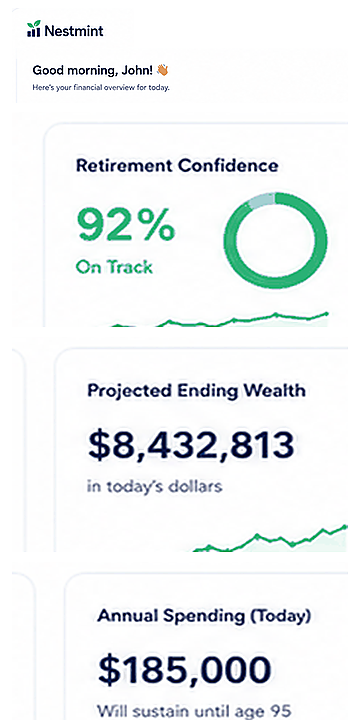

Here’s your financial overview for today.

Open Monte Carlo to calculate a modeled success rate.

Run the Retirement Planner to populate this metric.

From your current plan assumptions.

Run the Retirement Planner to populate this metric.

Run a simulation in the Retirement Planner to populate plan metrics and recommendations.

Open the Savings Estimator to set your ages, balances, contributions, and target — your growth plan appears here.

See how your savings today can shape your retirement tomorrow.

Enter your balances and contributions in the Savings Estimator — your projection appears here.

Run the Retirement Planner to activate your plan.

—

No income modeled.

Annual Spending

—in today's dollarsBased on the account balances in your current plan.

Run a retirement simulation to receive plan-specific next steps.

Run a simulation in the Retirement Planner to see projected annual spending by age.

From the current deterministic projection.

Run a simulation in the Retirement Planner to see projected annual taxes by age.

Summed per year from the same projected tax rows as the Lifetime Taxes metric.

Name the plan, then choose whether to use the guided planner or go directly to the complete assumptions area.

Please enter a plan name.

See how small, consistent savings turn into serious wealth over time.

Brokerage accounts, savings, CDs, etc. — taxed differently from retirement accounts.

Your gross annual employment income. Used to check Roth IRA eligibility, compute employer-match cap (if configured), and project your current-year tax bracket.

Money you save each month into a regular taxable brokerage account. Grows in its own bucket — no contribution limit and no employer match.

Traditional and Roth are your 401(k)/IRA contributions. The employer match below applies to their combined total (not to brokerage).

One rate for raises: it grows your contributions each year and your salary, so the employer-match ceiling below grows with your pay.

Match cap is computed against the Annual Salary in the Compensation section above, indexed each year by your Annual Increase. IRS rules (§401(a)(17)) cap matchable pay at $350,000 (2026, indexed). Leave both fields at 0 if you have no employer match.

Percentage of your contribution the employer matches (e.g. 50% = $0.50 per $1 you contribute).

Maximum % of salary the employer will match on (e.g. 6% means they only match up to 6% of your salary).

Traditional is the default and most common (employer match is pre-tax). Some plans offer Roth-match under SECURE 2.0 — you pay tax on the match amount in the current year but the balance grows tax-free.

Note: Salary is treated as fixed for the entire projection period. The employer match cap is based on the Compensation salary each year, even if your contributions increase annually.

Used by both Roth tools below — conversion math and contribution-bucket eligibility.

Used to personalize tool suggestions and milestone labels

Set different return rates for different year ranges.

Contributions are assumed to occur evenly throughout the year. Monthly is the most realistic for typical investments.

Target value renders from your saved goal in Goal Simulator.

Projected from current assumptions; not a guarantee.

Traditional + Roth + brokerage

Projected across the savings horizon

Across retirement and taxable accounts

Traditional, Roth, and brokerage balances — with the total — through retirement age.

The estimator preserves the four retirement-account buckets and taxable savings throughout the projection.

Use the estimate to begin spending, tax, healthcare, and withdrawal modeling.

| Timeline | Balances & Contributions | Investment Growth | Projected Outcome | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year | Age | Beg. Balance | Mo. Contrib | Annual Contrib | Empl. Match | Cumul. Contrib | Interest (Yr) | Cumul. Interest | End Balance | % From Growth | Real Balance (today's $) | Mo. Income @ 4% |

See how much free money you're leaving on the table. Enter your employer's match terms.

% of your contribution they match

Max % of salary they'll match on

Track when you'll hit key savings milestones. Based on your current inputs.

How should you split your annual retirement contributions across Roth IRA, Roth 401(k), Traditional 401(k), and Traditional IRA? See your capacity, allocate across the four buckets, and watch how the choice plays out over your time to retirement.

All three scenarios use the same contribution dollars, employer match, and growth rate, so the pre-tax balance is the same. Only the after-tax keep amount changes based on how the money is split between Traditional and Roth. Traditional balances are subject to required minimum distributions beginning at age 73–75; Roth balances are not.

Note: These projections cover retirement accounts only (Traditional & Roth 401(k) and IRA balances). Brokerage and taxable savings are excluded — see the Savings Estimator dashboard for your full total including non-retirement accounts.

Important: The lost tax deduction can represent a significant drag on the Roth advantage shown above. If a Traditional contributor were to reinvest those tax savings and let them compound over the full savings horizon, the result would partially offset Roth's edge.

Should you convert some of your traditional IRA/401(k) to a Roth before retirement? Pay tax now at your known bracket, then grow and withdraw tax-free. Reduces future RMDs and Medicare surcharges.

Once you stop working, income drops — but so does your control over it. RMDs starting at age 73–75 force withdrawals from your IRA whether you need the money or not, at ordinary income rates, in amounts that grow every year as your balance compounds.

The years between now and retirement are different. Your bracket is known. Your timeline is long. And every dollar you move to Roth now compounds tax-free for decades.

The question isn't whether to convert. It's how much, and when.

Federal + state, during conversion window

Federal + state, in retirement

See the cost of waiting. Compare starting today vs. delaying by 1, 3, 5, or 10 years.

Figure out how much to put into each account type based on your income and risk tolerance. Follows the classic priority order: get the employer match, then max tax-advantaged accounts. (2026 IRS limits)

If you're 50+, IRS rules let you contribute extra to 401(k) and IRA accounts. See how much more you could save. (2026 limits)

What if you had started saving with your current contribution plan 30 years ago? This compares your flat-rate projection against what actually happened in the S&P 500 — including the dot-com crash, 2008 financial crisis, and COVID. See how real market volatility would have affected your savings growth.

| Year | Annual Contribution | Cumulative Contributions | Total Investment Growth | End Balance |

|---|

| Scenario | Updated | Projected at retirement | Target | Status |

|---|

Explore different savings scenarios — solve for the missing variable.

Auto-filled from "Your Savings Today" — edit to override. Applies to all simulators below.

The total balance you want to reach. Seeds the cards below and powers the Savings Estimator goal-gap insight.

How much do I need to save each month to reach my goal?

How many years will it take to reach my savings target?

What annual return rate do I need to hit my savings target?

What will my balance be at a specific age given my current plan?

Tell us about you and your household.

This information helps personalize your plan and projections.

Your age as of today.

Age you expect to live to.

Number of years to include in this plan.

Tell us about your household and partner.

Age you expect your spouse / partner to live to.

Portion of pension or income that continues to survivor.

Expected spending as a % of pre-death spending.

Enter your account balances and key assets for the plan.

Fills these account balances from your Savings Estimator result. Uncheck to enter your own balances.

Enter your income sources for retirement.

Estimate your Social Security benefit.

Enter the monthly benefit amount used by the retirement engine.

Estimate your spouse / partner's Social Security benefit.

The spousal benefit is set automatically to 50% of your monthly amount.

The engine stores Social Security as a monthly benefit.

Add your defined benefit or other pension income.

Add spouse / partner pension income.

Add recurring employment or other income already supported by the planner.

Add spouse / partner employment income and contributions while working.

Contributed to the spouse's traditional account during the employment window.

Organize your retirement spending plan and major cash flow events.

Amounts are in today's dollars and increase with your inflation assumption.

When on, your Budget view's total keeps the annual spending amount in sync.

Define how your spending changes across retirement.

Phases are contiguous — each phase starts where the previous one ends. The last phase covers all remaining years.

Adjust spending when the portfolio crosses your selected guardrails.

Guyton-Klinger style: spending adjusts for inflation, then rises or falls when the withdrawal rate crosses a guardrail, within the floor and ceiling.

Add major planned events that impact your cash flow.

Add notes about your spending plan, assumptions, or anything important to remember.

Plan for healthcare costs in retirement.

Enter your expected annual healthcare costs by phase.

Estimate Medicare premiums and IRMAA surcharges using prior-year MAGI.

Medicare Advantage user? Set Medigap / Supplemental to $0; an explicit $0 is honored.

Used to estimate income-related monthly adjustment amounts.

We’ll use this history to project IRMAA brackets and surcharges.

Set your market return and volatility assumptions.

Choose how investment returns are modeled in your plan.

Returns compound geometricallyNominal annual return before taxes and withdrawals.

Each account class grows at its own nominal rate. Cash & Other is held at its entered value (no growth).

Phase rates apply to all accounts together — per-account rates aren't available in this mode. Your Blended / Per-Account choice is kept and applies again when you switch back to Fixed Rate.

Set your assumed volatility for market returns.

Taxable uses the profile above. Set Traditional and Roth overrides here when needed.

How often returns are compounded. Monthly (12x/year) is the most common default.

Set your tax profile and choose the strategy preferences that shape the plan.

How your ordinary income is taxed each year. The Automatic method applies the 2026 IRS brackets and standard deduction for your filing status, inflated over time; your state selection sets the state rate.

Used with the Automatic federal method. The flat method's state rate lives under Advanced.

Tax brackets and deductions grow at this rate in future years, as the IRS adjusts them for inflation.

Subtracted from income before tax. The default is the 2026 amount for your filing status; it inflates with brackets.

Extra deduction per person aged 65+, applied automatically in the years each of you qualifies.

Up to $6,000/person ($12,000 MFJ). Phases out at MAGI > $75K single / $150K MFJ.

Withdrawals from IRA/401(k) are always taxed as ordinary income. Check additional income types to include in your tax calculation.

The plan computes how much of your Social Security is federally taxable using the IRS provisional-income tiers (0%, 50%, or 85% of benefits depending on income). Leave this checked for realistic taxes — low incomes automatically produce $0 taxable SS. Uncheck only to model SS as fully tax-exempt.

Unchecking removes ALL pension income from the taxable-income calculation — use only if your pension is genuinely tax-exempt. If unchecked, lifetime tax will be significantly understated. Check the "Taxable Income" line after running.

When you sell in a taxable account, only the gain portion is taxed. The plan estimates that portion from your inputs below: with dynamic tracking on, it projects your gain % year by year from your cost basis; otherwise it applies the fixed gain % every year.

Progressive uses the real 0/15/20% LTCG brackets stacked on your income. Flat uses a single rate you choose.

Unused capital losses from prior years. Applied against gains first, then up to $3,000/yr against ordinary income.

% of your brokerage balance that is growth above your original investment today. Seeds dynamic tracking.

Projects your gain % each year as sales and growth change your basis.

Applied every year unless dynamic tracking is enabled.

Review the Brokerage Gain/Basis Estimator in the Deep Dive tab to see the year-by-year gain projection.

Choose whether the plan withdraws extra from your portfolio to cover taxes. When on, taxes never eat into your spending — and tax dollars taken from the IRA are themselves taxed, so the plan grosses the withdrawal up. When off, taxes come out of your annual spending amount.

Pays Roth conversion tax from the portfolio instead of reducing the converted amount.

The master switch for portfolio tax funding — when off, those taxes come out of your spending amount instead. The canonical control is a checkbox; the previous select could never fill (v149.507 correction to the v149.476 donor).

Choose how the engine takes distributions. RMDs are always taken first.

Computed from your birth year under SECURE 2.0.

Move money from Traditional IRA/401(k) to Roth. The converted amount is taxed as ordinary income in the year of conversion, but then grows and withdraws tax-free. Leave amount at $0 to skip.

The tax on each conversion follows your choice in "Paying the Tax Bill" above ("Fund conversion tax from portfolio"). Need a year-by-year schedule? Use the Roth Conversion Explorer in the Deep Dive tab.

Deliberately sells brokerage positions in low-income years to realize gains while your capital-gains rate is 0%, then reinvests — raising your cost basis so future sales owe less tax. The realized amount is capped by the Harvest Rate.

Max % of the brokerage balance realized per year.

Only needed with the flat federal method, or to change when withdrawals happen within each year.

When during each year withdrawals are taken — affects growth and tax sequencing.

Gain % used by progressive state-tax calculations when it differs from the federal estimate.

Review your plan before running the simulation.

All required sections are complete. You're ready to run the simulation.

This takes a few seconds. Your inputs stay editable afterward.

Model income, withdrawals, taxes, and spending — know exactly how long your money lasts.

Enter the benefit amount for the age you plan to claim. Find yours at ssa.gov/myaccount or on your annual SSA statement.

62 = reduced (~70%), 67 = full, 70 = max (~124%)

Annual cost-of-living adjustment. SSA historical avg ~2.5%. Set to 0 to model flat benefits.

Set to life expectancy for lifetime pension.

Age range for employment income.

Adjusted annually for inflation.

Define your own spending phases. Set the end year for each phase and the annual amount. The last phase covers all remaining years.

Spending adjusts dynamically based on portfolio performance. Set an initial spending amount and guardrail thresholds.

Initial spending is adjusted annually for inflation, then guardrails are checked. Based on the Guyton-Klinger dynamic spending approach.

Draw from brokerage accounts first, then traditional IRA, then Roth. RMDs are always taken.

When withdrawals are taken each year. Affects how much growth applies before money leaves the account. "Equal Throughout" models monthly withdrawals spread across the year.

One-time or multi-year extra withdrawals added on top of regular spending. Set From and To to the same year for a single-year withdrawal. Month controls when in the year the withdrawal occurs (affects growth).

One-time lump-sum deposits of after-tax money (e.g., home sale, inheritance, life insurance). Funds are added to your taxable account balance. Month controls when in the year the deposit occurs (affects growth).

Move money from Traditional IRA/401(k) to Roth. The converted amount is taxed as ordinary income in the year of conversion, but then grows and withdraws tax-free. Leave amount at $0 to skip.

Tip: Use the Roth Explorer strategy tool to find the optimal conversion amount, then enter it here to include it in your main projection.

Adds Medicare Part B, Part D, Medigap, IRMAA surcharges, and out-of-pocket costs to your annual spending. Costs grow at the healthcare inflation rate. IRMAA surcharges are based on your MAGI from 2 years prior (e.g., your 2026 Medicare premiums are determined by your 2024 income). For the first two years of your projection, NestMint uses the optional Prior Year MAGI fields below. If left blank, years 1–2 assume no IRMAA surcharge.

Set different return rates for different retirement phases.

Withdrawals from IRA/401k are always taxed as ordinary income. Check additional income types to include in your tax calculation.

Auto-set by filing status (2026 IRS amount).

$1,650/person MFJ, $2,050 single (2026). Only applies with standard deduction.

Up to $6,000/person ($12,000 MFJ). Phases out at MAGI > $75K single / $150K MFJ. Applies to both standard and itemized filers.

Determines tax brackets, standard deduction amounts, and LTCG thresholds.

Annual inflation adjustment for tax brackets, standard deduction, and LTCG thresholds. Set to 0% to use fixed 2026 levels. Historical IRS adjustments average ~2-3%.

Uses 2026 IRS tax brackets. Federal tax is computed progressively on taxable income after deductions.

Withdraws additional money from accounts to cover taxes on IRA/401k distributions, with gross-up when paid from IRA.

Also fund taxes on these income streams:

Withdraws additional money from accounts to cover taxes on selected income streams and Roth conversions, giving a more complete picture of account depletion. Note: paying conversion taxes from outside accounts is generally more efficient.

Taxes paid from brokerage first — IRA compounds without tax-funding draws.

Configure long-term capital gains tax rate, brokerage gain estimates, auto-harvesting, and loss carryforward.

Simulation results for your retirement plan

No simulation has been run yet for this plan. Run your first simulation to see projected outcomes, tax totals, RMD and IRMAA figures, and a side-by-side of withdrawal strategies.

Deterministic projections under your current inputs. Figures are modeled estimates, not guarantees.

Total portfolio value across all strategies.

Total portfolio value across all strategies — no percentile band.

Income = Social Security, pension, and employment. Spending = the plan’s spending need.

Distribution of accounts over time. Based on account balances.

Includes SS, pensions, withdrawals, and conversions.

Objective comparisons using the assumptions in your current retirement plan

Choose how strategies are ranked and run the engine using the assumptions in your current plan.

Tests combinations of withdrawal order, Social Security timing, and Roth conversion schedules — every candidate is a full plan simulation under your current assumptions.

Each finalist is then stress-tested across 500 seeded market paths — the same paths for every strategy — and ranked by the outcome lens you choose.

Advanced analysis, what-if scenarios, and strategy deep dives

See how different Roth conversion strategies would affect your lifetime taxes, RMDs, and ending net worth. The Explorer runs your full retirement simulation with and without conversions and compares the results. Tax on conversions is fully included — the converted amount is added to your taxable income each year, taxed at your federal + state rate, and reflected in all totals. A positive result means the upfront tax cost is outweighed by tax-free growth and lower future RMDs. A negative result means conversion costs more than it saves in your scenario — both outcomes are possible and the Explorer shows you which applies.

The core question is your tax rate today vs. your tax rate later.

Converting makes sense when your marginal rate during the conversion window is lower than the rate you'd pay on future RMDs. In that case, you prepay tax at a discount and all future growth is tax-free. The benefit compounds over 20–30 years and can be substantial.

Converting hurts when your current marginal rate equals or exceeds your expected future RMD rate. You'd be paying more tax today to avoid less tax later — a net loss that also compounds over time.

What drives the future RMD rate? Once large income sources like a pension or employment income end, your taxable income often drops significantly. Social Security and RMDs alone may put you in a lower bracket than you're in today — especially in the years before RMDs begin. That's typically where the opportunity lies.

What raises your current conversion rate? Pension income, employment income, and Social Security all stack on top of any conversion amount, pushing the marginal rate on the converted dollars higher. If your income is already high, conversions may land in the 24–35% federal bracket before state tax is added.

The Explorer below runs both scenarios for you and shows the actual dollar impact. Check the tax rate column to see what rate each strategy is effectively paying — and compare that to your projected RMD-year rate.

There is no IRS limit on how much you can convert per year. However, bigger is not always better. Key trade-offs:

The sweet spot — if one exists — is typically converting enough to fill your current tax bracket without jumping to the next one, or staying below the first IRMAA threshold. For some users, the optimal conversion amount is zero: if your income during the conversion window already exceeds your projected RMD rate, conversion increases lifetime taxes rather than reducing them. The Explorer's tax rate column shows the effective rate you'd pay on each strategy so you can compare it directly to your expected future rate.

These constraints apply only to "Compare Scenarios". IRMAA cap keeps MAGI below the first surcharge tier. Max bracket limits conversions. Min liquidity ensures brokerage stays above this floor.

Adjust assumptions and stress-test your retirement plan. Change return rates, life expectancy, inflation, SS timing, and spending to see how each affects your outcome.

How would your plan survive a major market crash? Pick a scenario, choose when the crash hits, and see the impact — including the recovery rally.

Run your retirement plan through 5,000 seeded market paths sampling annual returns around your expected return. Instead of one straight-line projection, see the modeled success rate and the range of possible outcomes. Same inputs always produce the same results.

Understand your effective tax rate in retirement and explore strategies to minimize lifetime taxes. Includes tax bracket analysis and the impact of relocating to a different state.

A sanity check on the Gain % you've entered in Tax Settings. Enter your estimated embedded gain today, and this tool projects how the blended gain % in your brokerage will actually evolve over time — accounting for fully-taxed RMD inflows (which arrive at 100% basis) and investment growth (which adds pure gain). If the projected line diverges significantly from your flat assumption, your cap gains tax estimates may be off.

Your best estimate today — check your brokerage statement for unrealized gain. Leave blank to assume 0% (no embedded gain on Day 1). Note: a higher % is more cautious from a tax perspective.

Comprehensive risk analysis with Monte Carlo success probability, tax burden, RMD exposure, and 5 more risk factors. Adjust the scenario sliders below to stress-test how changing assumptions affects your risk profile — without changing your main inputs.

What if you retired 30 years ago with your current balances? This shows how actual S&P 500 returns — including the dot-com crash, 2008 financial crisis, and COVID — would have affected your portfolio.

Compare different withdrawal sequences to see which order of drawing from your accounts preserves wealth the longest. Your current withdrawal order setting from the inputs above is highlighted.

Review your projected Required Minimum Distribution schedule starting at your RMD age (73 or 75, set by your birth year), based on your projected IRA/401(k) balance at that age (not your current balance). RMD amounts are calculated using the IRS Uniform Lifetime Table. See how RMDs grow over time, their tax impact, and strategies to reduce them through early withdrawals or Roth conversions.

Evaluate whether your planned spending is sustainable. See your effective withdrawal rate, how it compares to common benchmarks, and when adjustments might be needed.

Model Medicare premiums, IRMAA surcharges, Medigap supplements, and out-of-pocket costs through retirement. Healthcare inflation (~5.8%) outpaces general inflation — see how it compounds and what share of your spending goes to medical costs.

Compare claiming Social Security at different ages to see how each option affects your lifetime benefits, ending balance, and total income. Includes break-even analysis and COLA growth projections.

Cost-of-living adjustment applied each year. Historical average is ~2.6%.

Get age-appropriate asset allocation suggestions for your retirement accounts. See how shifting between stocks, bonds, and cash affects your projected outcomes over time.

See a visual timeline of key retirement milestones — from Social Security eligibility and Medicare enrollment to RMD start dates, spending phase changes, and projected fund depletion. Understand what happens at each stage.

A year-by-year breakdown of the first 10 retirement years: where your taxable income comes from, how the tax breaks down by type, and which account funded each tax dollar. Useful for spotting bracket-creep and brokerage-drain patterns.

Inspect the year-by-year simulation data, export to CSV for external verification, and review engine diagnostics. Useful for validating results against your own spreadsheet or tax preparer’s projections.

Explore projected estate outcomes, inherited-account tax treatment, beneficiary impact, and federal and state estate-tax considerations.

| Timeline | Portfolio | Income | RMDs & IRAs | Spending & Healthcare | Withdrawals | Taxable Income & Gains | Taxes | Cash Flows | Contributions | End-of-Year Balances | |||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Age | Year | Beg Bal | Growth ⓘ | SS Inc | Pension | Employ | RMD ⓘ | Exc RMD | Primary IRA Beg ⓘ | Spouse IRA Beg ⓘ | Spend Need ⓘ | HC Base | HC IRMAA | Spend W/D ⓘ | IRA → Spend ⓘ | Spcl W/D | Ord Tax Inc | Deduction ⓘ | Est Tax Inc | Brkt Room | Brkt Used | Roth Conv | Cap Gain | Cap L Used | Net Gain | Loss C/O | Base Fed | Base St | CG Tax | G-U Tax | Tot Tax | Spend W/D | Spcl W/D | Tax W/D | Tot W/D | Spcl Dep ⓘ | Contrib ⓘ | IRA/401k | Roth | Brokerage | End Bal |

Presentation: Spend Need is shown accounting-style — red parentheses denote a cash outflow. The underlying value is the plan’s spending target for the year; the CSV export carries the plain number.

Withdrawals: Spend W/D = withdrawal for living expenses. Spcl W/D = special withdrawal (also taxed). Tax W/D = withdrawal to fund taxes. Tot W/D = Spend W/D + Spcl W/D + Tax W/D. Spend W/D appears twice: once next to Spend Need (includes Spcl W/D) and again in the withdrawal math section (excludes Spcl W/D, shown separately).

Income & Tax: Ord Tax Inc = ordinary taxable income before deductions. Deduction = standard or custom deduction applied. Est Tax Inc = Ord Tax Inc − Deduction (estimated taxable income, ties to Tax Bracket Management). Roth Conv = amount converted from Traditional to Roth (included in Ord Tax Inc). Note: If the Enhanced Senior Deduction (One Big Beautiful Bill, 2025–2028) is enabled, you will see a step-down in the Deduction column in the first year after it expires — this is correct and reflects the provision's scheduled end date.

Bracket Fill (Tax-Smart): Brkt Room = how much IRA withdrawal room exists before hitting the target bracket ceiling (ceiling − base income). Brkt Used = actual IRA withdrawal taken to fill the bracket; this amount is included in Ord Tax Inc and taxed accordingly. If RMD exceeds the room, the excess is reinvested into brokerage. These columns are zero when not using Tax-Smart withdrawal order. Click any cell for the full breakdown.

Capital Gains: Cap Gain = gross capital gain from brokerage withdrawals. Cap L Used = capital loss carryforward applied against gains. Net Gain = Cap Gain − Cap L Used. Loss C/O = remaining capital loss carryforward.

Tax Computation: Base Fed = federal tax on ordinary income. Base St = state tax on ordinary income. CG Tax = Net Gain × LTCG rate. G-U Tax = gross-up tax from funding taxes via IRA. Tot Tax = Base Fed + Base St + CG Tax + G-U Tax.

Five focused steps. Your answers update the existing Savings Estimator automatically.

Add assets and debts outside your retirement plan to see your complete financial picture.

Retirement and investment accounts already entered in NestMint are included automatically.

Do not enter those accounts again here.

Only assets not already included in your NestMint savings or retirement accounts.

Enter current balances, not original loan amounts.

Optional. These entries calculate your broader net worth and do not change Savings Estimator or Retirement Planner projections.

Save to create your Asset & Liability Overview. You can update these values at any time.

A broader net-worth view kept separate from the assets used in your retirement projection.

Not yet saved

Save future updates to build your net-worth history.

Track every dollar in and out — whether it's a paycheck or a pension.

Monthly expenses by category

Review, export, and share the analysis already produced by your planning tools.

Headline projections, detailed annual results, and complete plan exports.

A shareable summary of assumptions, balances, income, spending, taxes, and projected outcomes.

Export the complete annual projection for further review in a spreadsheet.

Open the current plan's charts, account balances, taxes, withdrawals, and annual spreadsheet.

Explore factual differences among withdrawal approaches and inspect every calculation.

Compare withdrawal strategies against the same retirement-plan assumptions.

Open all detailed sections, including accounts, taxes, cash flow, healthcare, RMDs, Monte Carlo, and legacy analysis.

Review conversion comparisons, projected taxes, future RMDs, and ending wealth.

Generate focused reports from the other areas of your financial workspace.

Export the current savings projection, assumptions, and accumulation results.

Export income, expenses, savings rate, and multi-year budget projections.

Open beneficiary, estate-transfer, tax, and inheritance projections based on the current plan.

All your saved work in one place. Click any item to open it.

No saved scenarios yet

No saved scenarios yet

No saved scenarios yet

No other data